“The first panacea for a mismanaged nation is inflation of the currency; the second is war. Both bring a temporary prosperity; both bring a permanent ruin. But both are the refuge of political and economic opportunists.” — Ernest Hemingway (1899-1961), (September 1932)

“Armies, and debts, and taxes are the known instruments for bringing the many under the domination of the few.” — James Madison, (1751-1836), 4th U.S. President, (April 20, 1795)

“If the American people ever allow private banks to control the issue of their money, first by inflation and then by deflation, the banks and corporations that will grow up around them (around the banks), will deprive the people of their property until their children will wake up homeless on the continent their fathers conquered.” — Thomas Jefferson, (1743-1826), 3rd U.S. President

“We know now that government run by organized money is the same as government run by the organized mob.” — Franklin D. Roosevelt (1882-1945), 32nd American President, 1933-1945, (in a speech at Madison Square Garden, Oct. 31, 1936)

Don’t look now, but there is a new monetary craze going on in some parts of the world, and it is the new so-called ‘unconventional’ monetary policy adopted by some central banks to push interest rates to ultra-low levels, and even into negative territory.

For some time now, some central banks and some governments have been pushing nominal interest rates down, so much so that a few countries have negative short-term interest rates and, when inflation is factored in, even more deeply negative real interest rates.

Why suddenly such an unconventional monetary policy? Their rationale is a fear that the economy could otherwise be saddled with an overvalued currency and be faced with a too heavy debt burden, and this would hurt their economic growth.

How is this possible? How could a central bank push interest rates to zero or to below zero, and with what consequences? A central bank does that by offering zero or negative returns on private banks’ excess reserves or extra funds that those banks want to store at the central bank.

This is a complex matter, but essentially this occurs when private banks are awash with cash that they have trouble lending profitably to private borrowers.

They are then forced to find alternative ways to invest their funds, one of them is to park those funds at the central bank, or alternatively, to buy government bonds and other securities. The result is an increase in the prices of those assets and a lowering of interest rates.

The question to be asked is why many banks are saddled with too much excess cash, above and beyond what is required to meet the ordinary private demands for loans?

To answer that question, we have to go back to the international financial crisis of 2007 and later years.

This all began with the subprime financial crisis, which started at the end of the summer of 2007, when some mega-banks in the United States and in other financial centers were teetering on the edge of bankruptcy.

Indeed, they had created a new type of financial products, the so-called mortgage-and debt-backed securities (MBS) and other asset-backed paper (ABCP), which were bundles of risky debt and were sold as new esoteric securities.

When the housing market collapsed, these artificially created securities also collapsed, and the banks found themselves in financial trouble.

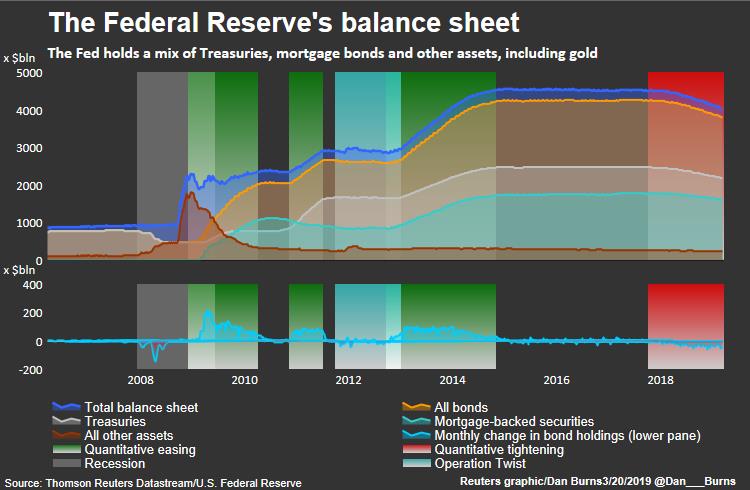

To prevent large banks from failing, the American central bank, i.e. the Fed, began printing new money to the extent of more than three thousand billion $ to rescue them.

The Fed called its generosity “Quantitative Easing” (QE), a fancy and innocuous word to cover the largest expansion ever of the monetary base in the United States, which is to a large extent made up of the Fed’s balance sheet (i.e. the private banks’ reserves held at the central bank) and of bank notes and coins circulating in the economy.

— With the newly printed money, the Fed bought Treasuries but also large amounts of private banks’ bad debts. And it did it for six years from 2008 to late 2014, in three successive rounds of money printing.

— Historically speaking, it was really an orgy of money printing. This was done, however, on the premise that the banks would leave most of their newly created bank excess reserves deposited at the central bank.

Nevertheless, the result (with so much excess liquidity in the system) was to push the prices of bonds and securities up and to lower interest rates across the board. And, in fact, interest rates have been declining ever since. The Fed said that it was ‘reflating’ the economy. In fact, what it was doing could be more accurately called ‘reflating’ the private banks’ balance sheets.

— During that period, the Fed’s own total balance sheet ballooned, jumping from roughly $1,000 billion in 2008, (ordinarily, it is mostly made up of Treasury securities and its net interest income is returned to the Treasury), to slightly more than $4,500 billion en 2017, an increase of 350 percent.

Today, the Fed’s total balance sheet is made up of Treasuries for about 55 percent, while mortgage-and-debt backed securities that it bought from the private banks account for about 40 percent, with gold and other assets accounting for the rest.

An important point is the fact that the Fed’s balance sheet before 2008 represented around 6 percent of annual U.S. output (GDP) but it reached 25 percent in 2014.

It has since declined somewhat to 20 percent of GDP, and the Fed would like to “normalize it “, i.e. shrink it further to prevent future inflation and above all, to be in a position to intervene if a new crisis were to arise.

{kind=link}

Let us now do some fast-forward thinking to today’s economic situation.

Enter the Trump administration in 2017 with its big increase in the pubic debt and with its bullying of the Powell Fed to bring down interest rates, possibly to zero

The last economic recession in the United States, (dubbed the Great Recession), was the worst since the Great Depression of the 1930’s. It began in December 2007, and it ended in June 2009. The economic recovery, however, has been the longest in U.S. history, having passed the 121-month mark, and it is already more than 10 years old.

The Trump administration’s economic policy as been characterized by trade protectionism, an anti-immigration policy, the lowering of taxes especially for large corporations and large banks, trillion-dollars yearly fiscal deficits, a very loose monetary policy, and a 13 percent jump in the total U.S. public debt since Jan. 20, 2017, when President Donald Trump took office.

[N. B.: The total national debt stood at $19.95 trillion on January 20, 2017. As of July 31, 2019, it has been galloping past $22.54 trillion.]

It could be expected that when the public debt has grown so large that there is fear that it could not be managed if interest rates were to rise. Governments and central banks would then be tempted to push interest rates down, in order to alleviate the burden of debt service (essentially interest payments on government bonds).

It is like imposing a stealth tax on savers and creditors.

It is worth pointing out that the Fed has recently done just that. Indeed, by artificially lowering interest rates below the inflation rate and a risk premium, it has made it possible for the U.S. Treasury to pay negative real interest rates on its public debt.

This means that when the inflation rate is higher than the nominal interest rate paid on the public debt, the U.S. government gets a free ride at the expense of its creditors.

If interest rates were to fall to zero, for example, or even to below zero, (as it is the case nowadays in Japan, after its two-decade long experiment with zero interest rates, and presently in some European countries, such as Switzerland, Germany, Netherlands, France, Sweden, etc.), savers, retirees, pension funds, insurance companies and lenders in general are the big losers.

Indeed, in countries where ten-year government bonds, for example, are generating a zero or a negative return, this means that the principle of compound interest has de facto been abolished for investors.

Such a development may have serious consequences for savers, retirees and pension funds.

However, when the central bank buys government bonds and issues newly created money in exchange, this is called “debt monetization”. If this is done on a large scale, it could eventually lead to a form of galloping inflation, possibly even to hyperinflation.

It is also worth noting that when central banks push interest rates to ultra low levels or to negative levels, investors have no other alternative than to purchase assets that offer positive returns, such as shares in companies or ownership titles of real estate.

Price bubbles in the stock market and in the real estate market can be expected to ensue. Such investments become a refuge from the negative returns received on fixed-income financial assets.

Historically, when this has happened, such developments have ultimately ended up in crashes and panics down the road.

The 1920s all over again?

The economic situation of today is, to a certain extent, reminiscent of the U.S. economy in the 1920s, leading to the Great Depression of the 1930s. Indeed, the U.S. economy had been growing by 2.7 percent per year between 1920 and 1929. There was overall full employment and inflation was stable.

Also, economic growth had been extended through protectionist measures, such as the Fordney-McCumber Tariff of 1922. During the presidential campaign of 1928, for example, republican presidential candidate Herbert Hoover (1874-1964) proposed large tariff increases on imports, as part of his platform.

Once in power, his promise was implemented with the passage of the infamous Smoot-Hawley tariff of 1930, which is thought to have accelerated the global economic depression.

The economy was also stimulated through increased spending on public works and through tax cuts in 1921, 1924, and 1925.

Moreover, President Calvin Coolidge (1872-1933) signed an anti-immigration bill called the Immigration Act of 1924, (also called the Johnson–Reed Act), whose main purpose was to prevent immigration to the United States of people from Asia.

There was also widespread hostility toward Catholic Americans, many of Italian origin, toward Jews, and toward blacks.

— These were the “roaring ‘20s”.

Considering the many similarities between the two periods, politically, socially and economically, a few questions beg to be asked: Is not history repeating itself? Might the excesses of today lead also to a day of reckoning? Might the current central bankers and politicians be leading the U.S. and other economies into a severe global economic downturn? Trade protectionism, lower taxes, higher debt levels, anti-immigration legislation, wholesale deregulation… etc.

— It’s ‘déjà vu all over again’!

Conclusion

Artificially low interest rates may be on their way in the United States. Fed Chairman Jerome Powell appears to have been intimidated by Donald Trump’s bullying tactics into lowering interest rates. Therefore, even though the U.S. economy is presently at full employment—partly a demographic consequence of the retirement in droves of baby-boomers—it is also saddled with very loose fiscal and monetary policies.

This is most unusual and it flies in the face of the principles of sound economic management. Such a situation is bound to create financial excesses and bubbles, to be corrected down the road.

In fact, the policy mix of today is a typical example of a government going after short-run economic and political gains at the expense of future medium- and long-run pains.

*

International economist Dr. Rodrigue Tremblay is the author of the book “The Code for Global Ethics, Ten Humanist Principles”, of the book “The New American Empire”, and the recent book, in French “La régression tranquille du Québec, 1980-2018“. He is a Research Associate of the Centre for Research on Globalization (CRG)

Please visit Dr. Tremblay’s site: http://rodriguetremblay100.blogspot.com/ where this article was originally published.

The original source of this article is Global Research

The 21st Century